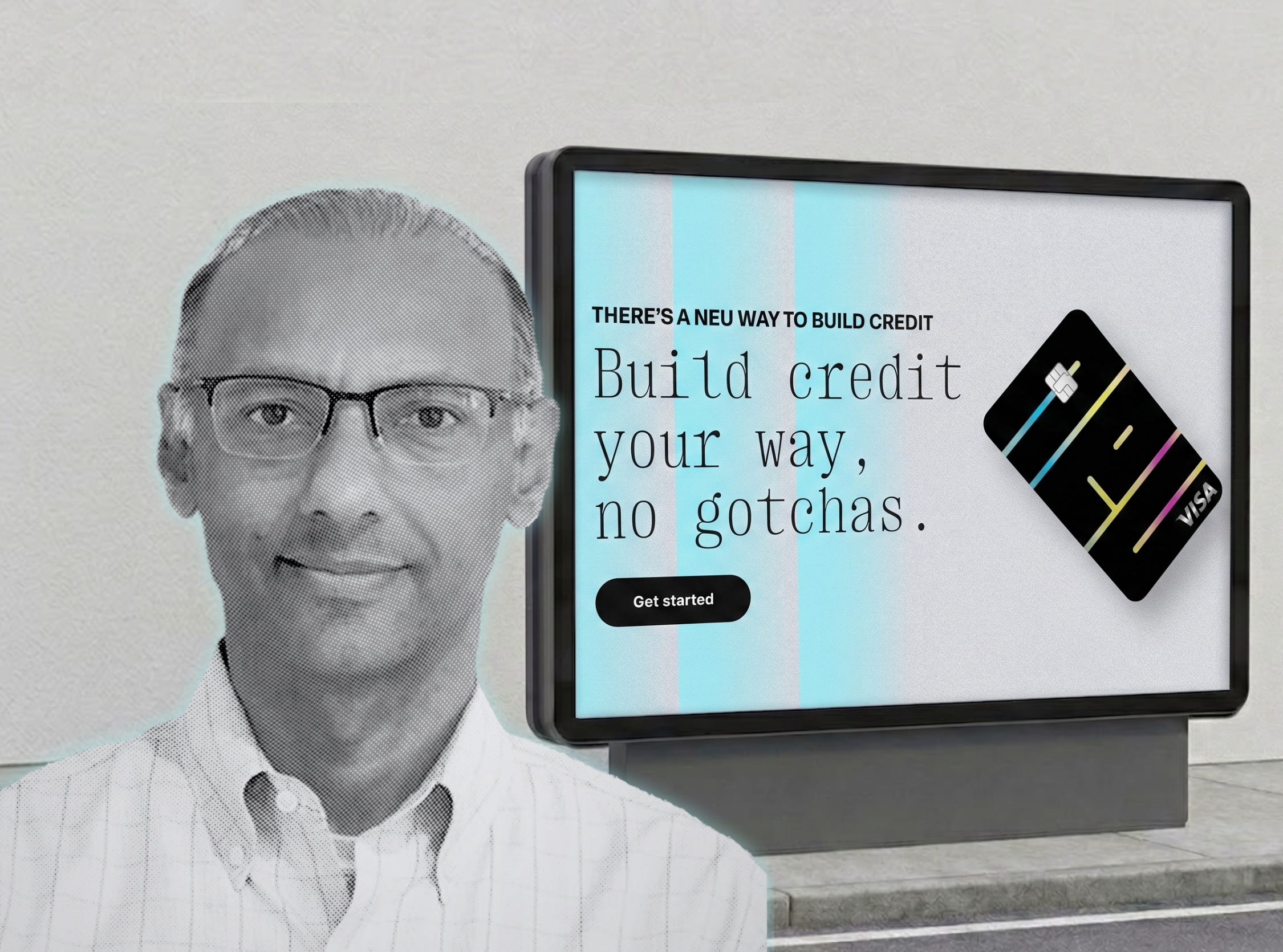

Yogesh Mehra - Neu Money

The Right Customer, Not the Easy One: Rethinking the Cost of Growth

When Demand Is Not the Problem

Neu Money’s credit card was nine months old when the affiliate channel started producing applications at a pace the team had not expected. The demand signal was there. Yogesh Mehra’s response was to slow down and look harder at who was actually applying.

“The demand is not the problem,” he says. “The right kind of demand is what we are optimizing for right now.”

Neu is a credit card built for two groups of underserved customers: people who are new to credit, including students, recent graduates, and recent immigrants; and people who have experienced financial hardship and are working to rebuild. In both cases, Neu can only deliver on its promise if the customer coming through the door is someone the product can genuinely serve. Volume without fit could weaken the unit economics and undermine the mission entirely.

That pressure, acute at any startup but more consequential here given Neu’s customer base, is where Yogesh’s marketing philosophy begins.

A Product Designed to Be Outgrown

“I did not have a credit card for many, many years,” Yogesh told us. “I have a chip on my shoulder and I want to do something about it.” The experience of being credit-invisible in a system that assumes everyone already has a score informs how he reads customer reviews, sits in underwriting meetings, and defines what a successful customer outcome actually looks like.

His path to Neu was a deliberate accumulation of builder experiences across institutions of very different sizes. At First Republic Bank, he was brought in to build and grow the marketing for Eagle Lending, an internal consumer lending fintech focused on professional loans and student loan refinancing, operating with startup-like velocity inside a large institution. When JPMorgan Chase acquired First Republic, Yogesh served on the transition team. Alongside his institutional roles, he built advisory and mentor relationships at both Techstars and Plug and Play, two separate startup accelerators, working with early and late-stage founders before stepping into a true founding-stage seat himself. “I thought I was ready,” he says of joining Neu.

“And we have done very well. But a true zero to one in a startup is unbelievably hard. It is pushing multiple boulders up the hill with little to no direction and little support. And that is very different from being in a startup role inside an established institution.”

Neu serves those two distinct customer groups through a framework Yogesh calls the graduation ladder: a defined progression from a thin or damaged credit profile toward a score that opens real financial options.

“What does success look like to the customer?” he asks. “Were we able to get customers there? Were we able to make a meaningful difference in the financial wellness of the customers over a certain period of time?”

The graduation ladder also explains why acquisition quality carries so much weight at Neu specifically. The product can only deliver on its graduation promise if the customer who comes in the door is someone whose profile the product actually fits. Acquiring the wrong customer does not produce a bad quarter. It produces a customer Neu cannot help, which defeats the purpose of the company.

The Quality Problem: Why Paying More Is Sometimes the Discipline

That framing puts a familiar industry concept in sharper relief. “The CAC trap is when you do not consider the quality of the vintage that you get from that channel,” Yogesh says. A channel can look efficient on the surface while delivering customers whose actual lifetime value (LTV) makes the economics deeply unfavorable. Optimizing for customer acquisition cost (CAC) alone measures the cost of acquiring a customer without accounting for the value that customer produces over time.

The correction, in Yogesh’s framework, is the LTV-to-CAC ratio: measuring the lifetime value of the customer relative to what was spent to acquire them.

“If you layer that dimension, you’ll make a very different decision... It’s totally okay to pay a little bit more to get the right kind of customer in the door. Even if you have to pay up a little bit, that’s the right trade-off.”

He extends that argument to paid acquisition as a long-term growth foundation. “Paid acquisition channels are an addiction and a tax on weak product defensibility,” he says. The channels themselves have become less precise over time, as third-party cookie deprecation limits targeting and privacy constraints tighten. The auction-based nature of digital media means that every competitor who throws budget at growth drives up costs for the whole market. In Yogesh’s observation, cost per thousand impressions (CPMs) have risen between 4% and 7% annually over the last decade.

“If your growth is coming from putting money in an auction, that’s not the best way to grow in the long term.”

The acquisition mix Yogesh is building at Neu favors channels with better structural durability. Third-party publications covering Neu offer higher credibility rather than the company promoting itself. “Somebody else talking about us is better than us talking about ourselves,” he says. App store reviews reflect the same sentiment, with customers writing that nobody took a chance on them before Neu did. For Yogesh, those reviews are both a brand signal and a measure of whether the graduation ladder is working.

Yogesh is also focused on where discovery itself is heading. He writes publicly about generative engine optimization (GEO), the discipline of ensuring a brand surfaces in AI-generated answers and large language model (LLM) outputs, not just traditional search rankings. His approach centers on earning credibility through third-party validation and building an authentic presence in the spaces where real financial conversations happen.

“Discoverability is very important,” he says. “Where discovery happens is going to shift over time."

Building the Team for What Comes Next

In his Substack article “5 AI Marketing Roles That No One is Hiring For (Yet),” Yogesh laid out a vision for how marketing departments will need to reorganize around artificial intelligence. He has since started building toward that vision at Neu, and his framework divides future marketing work into three lanes.

The first is human-led, covering strategy, ethics, judgment, and the fair lending guardrails that carry particular weight in a regulated fintech environment. The second is fully agentic, where AI handles programmatic media buying, landing page variations based on customer personas, and the orchestration of repetitive execution tasks. The third is a hybrid zone of co-creation, where humans and AI iterate together on creative concepts and messaging.

“Things that would have taken me three to four times as many people, we are doing right now because we have been able to orchestrate some of that work,” he says.

His approach to hiring reflects the same framework. As a guest faculty member at San Jose State University, Yogesh tells students the same thing he applies to his own team decisions. “Don’t focus too much on the tools. Focus on the frameworks, focus on the critical thinking, focus on the broader disciplines.” The concern running underneath that advice is specific. Leaning on AI too heavily, without maintaining genuine analytical effort, gradually erodes the thinking the tools are supposed to support.

“When I use AI too much without thinking too much, I feel like I get dumber over time and there are now conclusive studies to prove that.”

Graduation as a Growth Strategy

Neu's belief is that underserved credit customers deserve to be treated with the same respect and transparency as any other borrower from day one. When you lead with honest expectations and a clear path forward, the customer relationships that follow naturally become your strongest growth engine

“The best way to understand these customers is to go beyond the numbers and talk to them. Really understand what their day looks like.”

Transparency, the right product fit, and the graduation ladder make that possible. And for Yogesh, every acquisition decision, every channel trade-off, every debate about CAC and LTV, ultimately comes back to the same question: did the right person come through the door, and were we able to make a meaningful difference in their financial life?

More from Uncovered Media

| A guest post by

|